PhD Chapter - OECD report on promoting green finance and macroprudential

Posted by: admin 3 years, 2 months ago

(Comments)

The outline

- Introduction

- Risks related to climate change could destabilise the financial sector

- Some current macroprudential requirements may discourage investment in low-carbon instruments

- Macroprudential framework could be enhanced to support the green transition

- Conclusion

Introduction

The risks associated with climate change raise the spectre of a severe destabilisation of the financial system, and thus of the entire economy. This threat is leading a growing number of stakeholders in global finance to integrate an assessment of climate change into their risk management processes. The increased involvement of central banks and other macroprudential authorities, essentially by playing a coordinating role in the transition to a low-carbon economy, could accelerate this process. Already, central banks are increasingly integrating climate-related risks into their overall policy agenda, and some are starting to quantify those risks. Additionally, climate change considerations are increasingly shaping monetary policy strategy review and central banks’ reserve management. Some central banks have also said they will look at how macroprudential policy can help to mitigate climate change-related risks. In Emerging Asia, the central banks of Cambodia, the People’s Republic of China (hereafter ‘China’), Indonesia, Malaysia, the Philippines, Singapore, and Thailand have officially acknowledged the risks posed by climate change by joining the Central Banks and Supervisors Network for Greening the Financial System, established in 2017.

Notwithstanding these developments, more resolute and proactive action is needed from central banks in order to provide effective support for the transition to a low-carbon economy. The following section of this chapter discusses the challenges of incorporating climate-related risks into macroprudential regulatory frameworks, including potential methodological approaches for properly capturing and quantifying climate-related risks. It also reviews some of the elements of the current macroprudential framework that could hinder investment in climate-friendly projects. In doing so, it pays particular attention to the potential for minimum liquidity requirements to contribute to a spirit of short-termism. The section concludes with a reflection on the need to amend or expand the macroprudential policy framework in order to tackle climate-related systemic risks, and to support low-carbon investments. This includes setting out concrete examples of policy initiatives in this regard.

Risks related to climate change could destabilise the financial sector

Central banks’ mandates do not explicitly embed objectives related to climate change

Risks related to climate change were not treated with the same sense of urgency when central bank mandates were initially defined in the countries of Emerging Asia as they are today. Nevertheless, some rules and principles that define central banks’ remit, and state the limits of their responsibility to address future challenges such as climate change, are embedded in the mandates of several central banks in the Association of Southeast Asian Nations (ASEAN) (Table 2.1). The examples of the central banks of Indonesia, Malaysia, Myanmar, the Philippines and Singapore are very relevant, as their mandates embed support for the government’s economic policy, which includes sustainable growth. Cambodia’s central bank is also tasked, albeit in a less explicit manner, with conducting its monetary policy in a way that facilitates sustainable economic development, in line with the country’s overall economic and financial policy.

These underlying rules determine rather general obligations and limits on how each Emerging Asian central bank must contribute to the urgent need of tackling climate change. Central banks in the region should take decisive action wherever their financial-stability mandate overlaps with climate change.

Physical and transition risks related to climate change

The increasing severity and frequency of natural disasters stemming from climate change is likely to have an adverse impact on the financial sector, and indeed on financial stability. Risks to the financial system and to financial stability can be grouped into two broad categories. The first encompasses physical risks, while the second includes risks that stem from the transition to a low-carbon economy. Physical risk results from the direct impact of climate change on people and assets. When it materialises, physical risk could have three types of consequences for the financial sector. First, it could lead to an erosion of the value of the assets and collateral that have been pledged in credit transactions, when they are located in disaster-prone areas. The second type of impact is the increase in damage that must be covered by the insurance and re-insurance sector. Third, physical risk stemming from climate change could lead to a deterioration of local economic activity, which could then impact the solvency of borrowers.

In addition, the objective of mitigating climate change also exposes the financial sector to risks that are related to the transition towards a more sustainable economy. These risks may be broadly defined as the uncertain financial impacts on economic agents, both positive and negative, that will result from the implementation of a low-carbon economic model. Transition risks take several forms, namely: risks posed by policies aimed at decreasing greenhouse gas (GHG) emissions to meet the 2 degree target by the end of the century (e.g. carbon prices); legal risks arising as a function of climate litigation (e.g. in the context of climate damages); and technology risks that relate to the uncertainty in technological development and deployment. These risks are characterised by a very high level of uncertainty about the trajectory of the transition, notably the speed of reduction of greenhouse gas emissions, which will have a restructuring effect on the economy. Transition risk could have a material effect on the assets held by banking institutions, and on the investment side for insurance corporations. Table 2.2 summarises the major categories of financial impact from physical and transition risks.

Ultimately, there are a number of channels through which physical and transition risks could impact the financial system and financial stability. The impact of these risks will depend on the scale and scope of the actions that are implemented to tackle climate change, as well as on the speed of their implementation. In this regard, the Network of Central Banks and Supervisors for Greening the Financial System underlines in its progress report published in October 2018 (NGFS, 2018[3]) that the risks associated with climate change are a source of financial risk. It calls for central banks and supervisors to ensure that the financial system is resilient to these risks. Among the first recommendations issued by this network, in April 2019, was for microprudential supervision and the monitoring of financial stability to take account of the risks associated with climate change (NGFS, 2019[4]).

Owing to the challenges inherent in their quantification, there is currently little quantitative evidence of the impact of climate-related risks on the financial sector. However, the insurance stress test carried out by the Bank of England’s Prudential Regulation Authority in 2019 also integrated three types of climate-related scenarios (PRA, 2019[5]). The results of these stress tests provide an indication of the likely impact that the risks posed both by transition and by the physical impact of climate change may have on the investments of general- and life-insurance companies. In the case of physical risks, the impact ranges from -5% to -30%, depending on the sector, and assuming an orderly transition to a low-carbon economy by 2050. In the worst-case scenario, which assumes no transition, and a temperature increase of 4°C by 2100, the impact would be even more severe, ranging from -10% to -60% (Figure 2.1).

Figure 2.1. Estimation of losses related to physical risks for UK insurance companies, under different climate transition scenarios

Impact on investments in various economic sectors

Note: Scenario A describes a rapid and disorderly policy action with shock parameters set to hit in 2022. Scenario B describes an orderly transition, which assumes carbon neutrality in 2050. Scenario C assumes no transition and a temperature increase of 4°C by 2100. All three scenarios reference temperature targets that reflect different underlying greenhouse-gas emission pathways, and which are assumed to impact firms at different points in time (2022, 2050 and 2100).

Source: PRA (2019[5]), Life Insurance Stress Test 2019: Scenario Specification, Guidelines and Instructions, Prudential Regulation Authority, Bank of England, London, .

Some of these climate-related risks have started to materialise in several Emerging Asian countries. For instance, droughts have affected business operations in the Indian energy sector, while emissions regulations that apply to the chemicals sector in China have translated into lower operating rates at several chemical producers in the country (Box 2.1).

Box 2.1. Examples of the materialisation of physical and transition risk in selected Emerging Asian economies

Example of physical risk: Impact of droughts on the energy sector in India

Droughts have caused extreme water shortages, paralysing business operations in India. India faced acute rainfall deficiency over the period 2011-18. In this period, average rainfall exceeded expectations only in 2013. As a result, energy companies have seen an impact on their profits. According to the World Resources Institute, water scarcity forced 14 of India’s 20 thermal power stations to stop at least once between 2013 and 2016. This resulted in significant financial losses for energy producers. For instance, in one quarter a large power producer from India saw its earnings fall 17% due to water shortages.

Example of transition risk: Emission rules applicable to diesel vehicles in Indonesia

The Indonesian Ministry of Environment and Forestry requires all new diesel vehicles to meet Euro IV emission standards from April 2022. Individual carmakers voiced concern that the new emissions standards could lead to the accumulation of significant stocks of unsold vehicles, and to financial losses.

Example of transition risk: Emissions regulation affecting the chemicals sector in China

China’s National Action Plan on Climate Change (2014-20) stands as the main legislative framework that integrates climate change into the country’s environmental protection law. The chemicals sector has been affected by the forced relocation of plants away from urban areas, along with an overall reduction in the number of plants. There has also been considerable pressure to reduce energy consumption and emission levels. For instance, new emission taxes and limits for pollutants restrict air and water pollution from production processes. Many chemicals producers have had to operate below their capacity, while compliance with the applicable mandatory standards is strongly enforced by the Chinese government. For example, Chinese producers of caustic soda reportedly had to operate at 50-70% of capacity over 2017-18.

Source: AIIB/Amundi (2020[6]); Luo and Christianson (2018[7]); Suhartono (2020[8]).

The measurement of risks related to climate change poses various methodological challenges

The measurement of climate risk is still a developing field in the area of quantitative research. Even though climate risk intersects with the different categories of risk to which banks are exposed, such as credit, market, operational, and sovereign risks (Table 2.3), current models fail to capture climate risk in its entirety. For instance, climate-related risks can lead to credit risk as they can cause deteriorations in both borrowers’ ability to repay their debts, and in banks’ recovery rates. There is also a prospect of market risk, in that a sharp correction in valuations of assets such as equities and commodities may occur in the scenario of an abrupt transition to a low-carbon economy. Similarly, legal and reputational risk are the two main categories of operational risk that banks face due to climate-related uncertainty. It is necessary, therefore, to consider changing risk models in order to integrate climate-related issues. Moreover, it is also necessary to look at making climate risk a fully-fledged element of banks’ risk-management strategies.

Capturing physical risk in banking risk models is a methodological challenge. A natural disaster can cause a borrower to fail. However, credit risk models are ill-equipped to anticipate such strongly-correlated events. In the event of a localised natural disaster, such as a flood or an earthquake, the correlation between default events is primarily a geographical one. The correlation is more difficult to capture in the case of a non-localised natural disaster, or a localised disaster with broad effects, such as a pandemic or heat wave. For a comprehensive approach, one would need to identify the idiosyncratic vulnerabilities of each counterpart to climate risk. However, the effects of physical risk are complex to anticipate, each type of event giving rise to a specific scenario. In the case of physical risk, the coverage rate of a population or territory by flood, storm, or earthquake-type insurance is, therefore, a factor that has a direct impact on credit risk. If losses are insured, more frequent and severe weather events first affect insurance and re-insurance companies. Then, indirectly, they affect their customers through higher premiums. If losses are not insured, the burden falls on households, businesses and, ultimately, on government budgets.

In a joint report, the Bank for International Settlements and the Banque de France have compared climate risk to a “green swan” (Bolton et al., 2020[10]). Indeed, and as touched upon already, climate change has specific characteristics that make its impacts difficult to model. First of all, the use of historical data is of little use in measuring future risks, as physical risks will worsen with global warming, and transition risks remain low for the time being, as policy actions are still at an early stage at the global level. Second, the changes induced by climate change will be far-reaching, with non-linear, correlated, and potentially irreversible impacts. Third, the different time horizons at which the various effects of climate change will materialise are uncertain, whereas the likelihood of these changes occurring is high. Finally, the extent of long-term changes will depend on short-term policy actions.

As a result, a value-at-risk-type representation will therefore only imperfectly capture climate risk, which is typically positioned beyond the 99% confidence interval. Given its unprecedented nature, climate risk (and in particular transition risk) seems to be more compatible with a forward-looking approach based on scenarios, than with statistical models, which are necessarily based on historical data. Physical and transition risks represent two distinct types of risk, which must be handled differently, because they have different characteristics and channels of transmission to the banking sector.

The climate stress test undertaken by the central bank of the Netherlands, which was the first exercise of its kind, provides an initial methodological reference framework upon which to build. It is also more holistic compared to other stress tests, in that it tries to better assess the offsetting benefits of the transition. The climate stress test of the Dutch central bank was built around three shock scenarios. Under the technological shock scenario, unanticipated technological breakthroughs make it possible to double the share of renewable energy in the energy mix. Under the regulatory shock scenario, a set of policies aimed at reducing greenhouse gas emissions is implemented abruptly, resulting in a sharp increase in the price of carbon. The third scenario is that of a confidence shock, in which uncertainty about the government’s climate change policies causes a sudden drop in confidence among consumers, producers and investors (Vermeulen et al., 2018[11]).

The transition to a low-carbon economy requires a major investment effort, in particular, to allow the reduction of greenhouse gas emissions, and to ensure the resilience of energy systems to climate change. The squeeze that COVID-19 put on fiscal headroom in Emerging Asian countries, with the pandemic occurring in a context of already rising levels of government debt, makes it even more imperative to mobilise private capital for the transition to a low-carbon economy. Moreover, increased government spending to address the health and social impact of the pandemic, in addition to the economic impact, implies that governments in Emerging Asia have even fewer resources available to meet the sustainable development goals (ADB, 2021[12]).

However, the private sector alone may not have the capacity to contribute to this goal without support from policy makers. There are several reasons why the financial sector is unable to make its activities greener without public intervention. More precisely, many green investment projects do not provide their promoters with sufficient returns to obtain immediate financing. It is, therefore, a prerequisite to internalise the social costs. In terms of external financing, markets are imperfect, and the fixed costs are significant, making it difficult to set up long-term projects. In addition, the high degree of environmental, economic, and regulatory uncertainty renders the risk assessment process challenging. This, in turn, deters investors further. Moreover, a preference among investors for liquid assets and short-term investments is detrimental to the financing of green assets. This explains why, for green investments, bank financing generally predominates. In China, for example, green lending has increased substantially over recent years. The share of green credit in the total assets of the Chinese banking sector grew from 0.6% in 2007 to 3.2% at the end of 2016 (Volz, 2018[13]). Green bonds are another important financing source for climate-friendly investments. While green bond issuance in the Asia-Pacific region has grown since 2016, it still trails volumes issued in Europe and North America (Box 2.2).

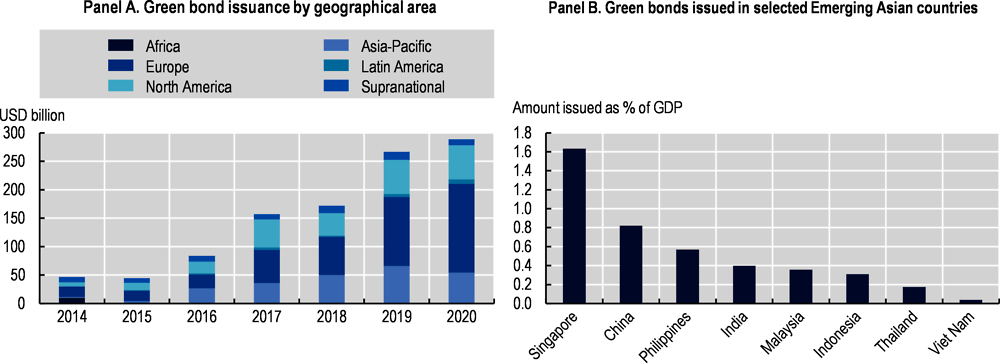

European green bond issuance led the way in 2020, amounting to a combined total of USD 156 billion. Asia-Pacific issuers accounted for USD 53.2 billion, or 18.4%, of global green bond issuance in 2020 (Figure 2.2, Panel A), despite issuance declining in the region from USD 65.1 billion in 2019. There was limited green bond issuance beyond Europe, North America, and Asia-Pacific in 2020. At the country level, the largest green bond issuance in 2020 relative to domestic GDP took place in Singapore (1.6%), followed by China (0.8%) and the Philippines (0.6%) (Figure 2.2, Panel B).

Corporates, both financial and non-financial, were the strongest contributors to green bond issuance in 2020, continuing a trend observed in 2018 and 2019 (Figure 2.3, Panel A). Non-financial corporates issued USD 64.7 billion in 2020, or 22.2% of the total, while financial corporates issued USD 55.6 billion, equivalent to 19.1% of the total. When the corporate sector is excluded, government-backed entities registered the highest total in 2020, with 22.1% of total issuance. In terms of how the proceeds are used, energy and buildings continued to lead in 2020, with 35.8% and 26.6% of total issuance respectively (Figure 2.3, Panel B). Transport continued to be the third-highest category, at 23.2%, followed by water projects, which accounted for 6.5% of issuance.

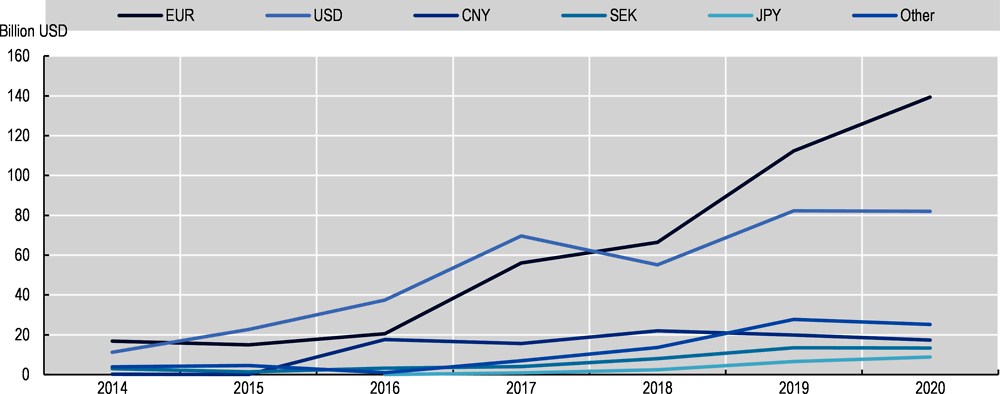

Figure 2.4 provides information on the currency distribution of green bonds that have been issued. It reveals that the bias towards the euro is very pronounced, as nearly 49% of green bonds issued in 2020 were denominated in euros. Nearly 29% of green bonds were denominated in US dollars, while 6% were denominated in Chinese Yuan renminbi, and 4.6% in Swedish krona. Relating the total green bond issuance by geographical area (Figure 2.2, Panel A) to the currency mix provides an indication of home bias in issuance.

According to a report by the International Finance Corporation, the share of climate-smart lending in banking institutions’ total claims on the private sector in 2016 ranged from 5% in India, Indonesia, the Philippines, and Viet Nam, to 7% in China (Figure 2.5). Among countries for which such forecasts are available, China also displays the highest potential for climate-smart investment over the period 2016-30, estimated at USD 15 trillion. India ranks second, with an estimated potential in this regard of USD 3 trillion, followed by Viet Nam with USD 753 billion, Indonesia with USD 274 billion, and the Philippines with USD 115 billion (Figure 2.5). In order to accommodate the debt financing for the climate-smart investment opportunities that have been estimated, however, the share of banks’ loan portfolios that is dedicated to climate-related lending would have to shift significantly through to 2030, from an estimated 5-7% at present, to around 30% of total bank lending (IFC, 2018[14]).

Some researchers have argued that macroprudential policies implemented in the aftermath of the global financial crisis, most notably the Basel III package, tend to promote short-term brown projects, to the detriment of more long-term, climate-friendly investments. For example, Gersbach and Rochet (2012[15]) conclude that, with the financial sector in competitive equilibrium, banks offer privately optimal contracts to their investors, but these contracts are not “socially-optimal”. Similarly, Thanassoulis (2014[16]) notes that a regulatory pay cap in proportion to assets could alter banks’ risk, value, and asset allocations. Moreover, the cap is shown to reduce banks’ risk-taking behaviour (Thanassoulis, 2014[16]), which could have a negative impact on their willingness to finance long-term and risky low-carbon investments.

Other studies note that, in particular, liquidity requirements might have a negative impact on banks’ willingness to finance climate-friendly investments. Indeed, Narbel (2013[17]) notes two distinct aspects of the Basel III framework that could reduce their appetite for funding renewable energy via project finance. First, long-term financing is likely to become more expensive because of liquidity metrics such as the liquidity coverage ratio and net stable funding ratio. Second, the new capital requirements in Basel III imply that banks will have less-ample funds to invest in illiquid assets. The impact on capital-intensive renewable energy technologies could be harder than for other technologies, due to their inherent characteristics, such as shorter proven track records, higher capital costs and longer-term financing needs (Narbel, 2013[17]). Relatedly, Spencer and Stevenson (2013[18]) argue that the Basel III financial framework, and in particular the minimum liquidity requirements, could reduce banks’ capacity to provide long-term credit. Some of the implications of capital and liquidity requirements for the low-carbon sector are illustrated in Table 2.4.

The existence of climate externalities and failures in financial markets could justify the use of financial regulation to combat climate change. In this connection, different regulatory instruments can be used to address the challenges of climate change (Table 2.5). For macroprudential policy, preserving financial stability may require the use of new macro-surveillance instruments, such as climate-related macro-stress tests. It could also involve the use of specific macroprudential regulatory tools, such as a capital conservation buffer, a counter-cyclical capital buffer, sectoral exposure rules, or loan-to-value caps. The following section provides an overview of potential solutions for greening the existing macroprudential policy framework. It also addresses the need to establish a standardised taxonomy for green assets at the regional or even global level, which is a pre-requisite for the effectiveness of green macroprudential policies.

Integration of risks related to climate change into macroprudential stress tests

An effective framework for monitoring systemic risks is an essential element of the macroprudential toolkit. Among the wide range of risk indicators, moreover, macroprudential stress tests play a key role. For years, national supervisors and the International Monetary Fund have conducted stress tests on the banking sector, or indeed the entire financial sector in a given country, to quantify the systemic impact of deteriorating macroeconomic conditions. Such stress tests also take into account the interactions between a deteriorating situation in the financial sector and the real economy. To account better for systemic climate risk, it is necessary to integrate the impact of climate change into these macro-stress tests. Some exercises have already been carried out. For example, researchers from the Netherlands central bank assessed the impact of a selection of transition scenarios on the country’s financial sector, concluding that the impact would be significant (Vermeulen et al., 2018[11]).

Climate stress tests are typically based on macroeconomic models that are capable of integrating climate change so as to determine its impact on macroeconomic variables. Given the complexity of the links between climate change, climate impacts, and socio-economic conditions, such an exercise requires sophisticated modelling. Calibration is also proving particularly difficult, given the lack of historical data on the impact of climate change. Overall, then, climate stress tests face major challenges. First, they need to take account of both physical and transition risks. So far, however, the focus has mostly been on the latter. Second, the definition of scenarios is another major challenge. Scenarios should be plausible, but also sufficiently severe, in order to be meaningful for all financial institutions within a jurisdiction, for the sake of comparability, or at the international level, to ensure a level-playing field. They should, moreover, focus on relevant risk factors, namely the channels through which climate risks will affect both the counterparties of financial institutions and the financial institutions themselves. Another difficulty relates to the gap between the short-term horizon of the typical stress test exercise and the medium to long-term horizon of climate risks. Longer-term horizons would also benefit from taking into consideration policies to mitigate such impacts, in order to better inform financial stability and fiscal policy initiatives.

Several major jurisdictions have already announced climate-related stress tests, and several others are considering undertaking them (Table 2.6). In Emerging Asia, methodologies for stress testing climate change-related risks are still at an early stage. The Monetary Authority of Singapore has already started to stress test for climate risks, but only in the insurance sector. In its 2018 industry-wide stress test exercise, it subjected insurers to a scenario involving extreme flooding, requiring them to consider the impact on their balance sheets of higher claims from damage to insured property. In addition, it is working towards incorporating a broader range of climate-related risks in thematic scenarios for its future industry-wide stress tests (MAS, 2020[19]). In April 2021, meanwhile, China’s central bank announced that it would work with other financial regulators to develop a methodology for climate-related stress tests, and would conduct such exercises in due course.

Given the complexity of climate stress tests, macroprudential policy makers could envisage alternative short-term solutions, such as scenario analysis. This is a less comprehensive exercise that could be used to assess the sensitivity to selected parameters of banks’ profit and loss accounts, and the items on their balance sheets. The level of these parameters is not derived from a macroeconomic model. The Task Force on Climate-related Financial Disclosures issued several recommendations in its 2017 report (TCFD, 2017[2]) on how to incorporate scenario analysis into strategic planning processes. The first recommendation is to further develop scenarios of transition that would keep global warming to two degrees Celsius or lower, that can be applied to specific industries and geographies, along with supporting outputs, tools, and user interfaces. The second recommendation concerns the development of broadly accepted methodologies, data sets, and tools, to allow organisations to undertake scenario-based evaluations of physical risks. Another recommendation is to make these data sets and tools publicly available in order to facilitate their use by organisations, reduce organisational transaction costs, minimise gaps between jurisdictions in terms of technical expertise, enhance the comparability of climate-related risk assessments by organisations, and help to ensure comparability for investors.

Existing macroprudential policy instruments could be amended to support green finance

When considering how to use existing macroprudential policy instruments to address the risks of climate change, the most relevant instruments could be those that target credit growth directly, or indeed those that target the sectoral allocation of credit. Examples of the former include capital buffers for risk-weighted assets. Examples of the latter include large-exposure rules that apply to potentially encumbered assets. Moreover, the Basel III counter-cyclical capital buffer could be particularly useful for promoting financial stability while transitioning from a high-carbon to a low-carbon economy, assuming there is an analogy between “financial bubbles” and “carbon bubbles”. Instruments targeting specific categories of loans, such as loan-to-value and debt service-to-income caps, could also be considered. However, their impact would, by definition, be limited to a specific sector. For example, it would be limited to the real estate sector in the case of loan-to-value and debt service-to-income caps. In the same vein, specific requirements targeting leverage ratios could be considered as a macroprudential policy response to risks related to climate change. However, the effectiveness of limiting bank indebtedness by regulating credit growth should be compared to that of implementing specific capital buffers.

Capital requirements could indeed be used to address climate-related risks. For example, a climate adjustment factor could be used to modify the risk weights of assets depending on how they affect the transition to a low-carbon economy. This could be achieved either by applying lower risk weights on green assets, or by increasing the risk weights applicable to so-called brown assets, whose carbon intensity is relatively high. One challenge to the integration of climate-related elements into capital requirements is the lack of sufficient evidence of a risk differential associated with green products. A more in-depth assessment of risk differentials associated with sustainability and climate risks will therefore be necessary before such capital adjustments become widespread practice (OECD, 2020[21]).

Another type of requirement that could be used is the leverage ratio. Introduced as part of the Basel III framework, this tool aims to limit each bank’s overall leverage. The leverage ratio could be supplemented with a sectoral leverage ratio requirement that imposes stricter rules for assets with high-carbon intensity. Further research would be needed to evaluate the effectiveness of such a policy tool as compared to minimum capital requirements. This research would also need to take into account the difficulties of implementation.

Liquidity requirements represent another type of requirement that could be amended in order to promote the transition to a low-carbon economy. Under Basel III, banks are subject to a short-term liquidity ratio, which requires banks to hold a certain level of short-term assets. They are likewise subject to a long-term structural liquidity ratio, which requires that long-term assets be financed by instruments with a maturity above one year. As has already been discussed with regard to capital requirements, liquidity requirements as they currently stand could hamper the financing of green activities, by making long-term financing more expensive. Regulators could consider differentiating these liquidity requirements to account for climate change, in order to give preferential treatment to green assets over brown assets. From a risk perspective, more in-depth research is necessary in order to understand whether green assets do indeed pose lower liquidity risks compared to other types of asset on banks’ balance sheets. From an economic policy perspective, meanwhile, applying differential treatment for green versus brown assets could facilitate the financing of green activities, and slow that of brown activities. Putting aside the question of the taxonomy that is needed to identify green and brown activities, evidence of the effectiveness of such a policy is still lacking. More research is therefore required in this area, before policy makers could implement any binding requirements.

Exposure limits and credit ceilings constitute the last group of tools that could help to promote and manage the transition to greater sustainability. Rules on large exposures typically set limits, usually a certain percentage of capital that individual loans cannot exceed. Concentration limits, meanwhile, usually set a given percentage of capital that the total amount of large loans cannot exceed. The aim of such limits is to force banks to diversify their loan portfolios in order to better withstand the bankruptcy of a large individual company, or a group of large companies. Concentration limits could be applied to overall levels of investment in carbon-intensive assets, which would be highly sensitive to a sharp transition to a low-carbon economy. As regards credit ceilings, limiting the expansion of bank lending to certain industries, and investments in certain specific asset classes, could also reduce financial flows to sectors or companies that exceed given carbon emission targets.

Specialised research has devoted attention to the need for macroprudential frameworks to evolve in order to improve the management of risks linked to climate change. Still, no consensus has emerged on the best way forward. Several studies have explored ways to amend central bank mandates so that they would include instruments that could support the transition to a low-carbon economy. For instance, Batten, Sowerbutts and Tanaka (2016[22]) explore the impact of climate change on the monetary and financial stability objectives of central banks, and identify several ways in which climate change, and policies on carbon emissions, could affect them. First, a weather-related natural disaster could trigger financial instability and a macroeconomic downturn if it were to cause severe damage to the balance sheets of economic agents. Second, climate change could have longer-term implications by affecting an economy’s potential growth rate. Third, a sudden and unexpected tightening of policies on carbon emissions could give rise to transition risks, in the sense that a disorderly re-pricing of carbon-intensive assets may generate a negative supply shock. Finally, increased reliance on bio-energy could increase the volatility of food and energy prices, thus making it more challenging for central banks to keep inflation close to their targets (Batten, Sowerbutts and Tanaka, 2016[22]). Batten, Sowerbutts and Tanaka (2016[22]) also argue transition risk could be mitigated through transparent, predictable and forward-looking policies on carbon emissions that encourage an early redirection of private investment towards low-carbon technologies.

Elsewhere, Dikau and Volz (2018[23]) list additional ways in which the macroprudential policy framework could be amended or enhanced to support climate-friendly investments. For instance, climate-related stress tests could help to calibrate green macroprudential policy instruments, and to facilitate the incorporation of the vulnerabilities that the tests identify into capital buffers, risk weights, and caps. In addition, capital requirements could be calibrated to differentiate asset classes based on sustainability criteria. Capital surcharges could be applied for institutions with large exposures to carbon-intensive assets, altering the identification of systemically-important financial institutions to take account of their systemic impact on the climate. In anticipation of sudden and negative price developments that may transpire in the future, higher risk weights could be assigned to carbon-intensive assets. Furthermore, loan-to-value and loan-to-income caps, or restrictions on large exposures, could be deployed in order to limit the amount of credit that banks extend to certain sectors, counterparties or geographical areas (Dikau and Volz, 2018[23]). Some of these proposals are in line with Schoenmaker and Van Tilburg (2016[24]), who identify capital instruments such as increases in risk weights, as well as restrictions on large exposures, as the most promising prudential instruments for carbon-intensive assets.

In a similar vein, D’Orazio and Popoyan (2019[25]) focus on the financial regulatory instruments that can be implemented within the existing regulatory framework. The authors argue that many existing policy interventions and proposals, such as the net stable funding ratio and the liquidity coverage ratio, run the risk of creating destabilising effects for the financial sector. Therefore, the authors suggest a set of alternative strategies to “greening” the existing Basel III requirements (Table 2.7). For example, the capital requirements toolkit could be expanded with a counter-cyclical, or negative, capital buffer over the course of the “carbon-intensive” credit cycle, favouring financial stability and mitigating excessive credit growth to brown projects. Second, leverage and liquidity requirements could be amended through the implementation of a sectoral leverage requirement. This could help to channel lending towards a specific green sector. Moreover, liquidity regulations could also discourage short-termism in financial intermediation. Minimum or maximum credit floors or ceilings, and large-exposure limits to constrain banks’ funding of brown sectors, are additional measures that could be considered.

While the implementation of green macroprudential policies could yield numerous benefits, certain factors may also constrain their effectiveness. As Bolton et al. (2020[10]) discuss the European Union’s experience with its SME Supporting Factor policy, which reduces capital requirements for lending to small and medium-sized enterprises. This EU policy uses similar levers to those that have been reviewed as potential amendments to macroprudential policy frameworks with regard to climate change. However, it has not been successful in triggering major changes in banks’ lending to SMEs. Furthermore, the implementation of a green macroprudential policy could potentially lead to trade-offs between the short- and long-term stability of the financial system. This is due to the mismatch between the long-term desirability of rapid and extreme measures to accelerate the transition to a low-carbon economy, and their potential to have a destabilising effect in the shorter term. As also argued by Bolton et al. (2020[10]), the main challenge in the short run is not the cost of green projects, but their number, which the authors still consider insufficient to drive real change.

Examples of policy initiatives to promote the transition to a low-carbon economy

In Emerging Asia, several countries have taken decisive action towards developing green policies (Table 2.8). For instance, India’s central bank imposes lending quotas in order to make sure that a minimum proportion of bank lending flows to environmentally-friendly sectors. It has issued guidelines on priority sectors for lending, in order to encourage and support environmentally-friendly lending by commercial banks, which in turn helps to achieve the United Nations Sustainable Development Goals. Eight priority sectors have been identified, one of which is renewable energy. The guidelines require domestic commercial banks, plus foreign banks with 20 branches or more, to make sure that loans to the eight priority sectors constitute at least 40% of their adjusted net bank credit, or credit equivalent of off-balance sheet exposures, whichever is higher (RBI, 2020[26]). Elsewhere, Malaysia’s central bank published an impact assessment framework for value-based intermediation financing and investment in 2020, with sectoral guidelines on palm oil, renewable energy, and energy efficiency. Also in 2020, it began a pilot implementation of its Climate Change and Principles-Based Taxonomy (Table 2.8). Moreover, China’s central bank and banking regulatory commission have developed a series of green credit guidelines, requiring banks to establish a monitoring and evaluation system for green credit (Park and Kim, 2020[27]). This progress notwithstanding, Emerging Asian policy makers have yet to implement specific green policies in the macroprudential area.

A reflection on the role of prudential regulations in promoting the transition to a sustainable economy is also already well underway in the European Union. The EU’s banking authority recommended in 2019 that legislators integrate sustainability considerations in directives and regulations that apply to the banking sector, in particular where they relate to governance and risk management. Additionally, it emphasised that the calibration of prudential requirements, which are primarily based on historical data, may not be a sufficient means to assess future changes, which may be without precedent. It pointed to the need for an enhanced, dynamic and forward-looking perspective in areas such as the calibration of prudential requirements, and approaches to modelling. As it seeks to incorporate environmental, social and corporate governance (ESG) factors in the prudential regulation applicable to banks, the aim is to ensure that there is no bias towards unsustainable financing (EBA, 2019[29]).

With specific regard to the transition to a low-carbon economy, central banks and other financial regulators around the world have implemented a range of policies. Campiglio et al. (2018[30]) provide a summary of these interventions (Table 2.9). For example, in 2011 Brazil’s central bank extended its requirements for the internal capital-adequacy assessment process that stems from the second pillar of the Basel II accords, by requiring commercial banks to take into account their exposure to environmental risks. More specifically, commercial banks are requested to incorporate these issues into their lending strategies, to carry out environmental stress tests, and to publish annual reports outlining their methods for assessing risk and exposure to social and environmental damage. These practices could serve as a benchmark for macroprudential policy makers in Emerging Asia.

Finally, the need to improve the comparability and quality of data with which to assess climate-related risks and opportunities is apparent. Non-financial reporting directives in a range of countries could serve as an example. The need to improve data comparability and quality ranks high on the G20 Sustainable Finance Working Group’s agenda, with the Financial Stability Board conducting work on this topic. The OECD has also raised the need for better quality reporting on climate-related factors, highlight that effective market pricing of climate transition is hampered by insufficient data, including financially material metrics and analytical tools to measure and manage climate transition risks, and lack of policy clarity regarding carbon pricing and support for renewables.

The development of a green taxonomy is a prerequisite for effective green macroprudential policy

Implementing green macroprudential regulation implies being able to distinguish with certainty between green and brown projects, and also those that are neutral with regard to climate change. The development of a stable, clear and standardised taxonomy in as many countries as possible is, therefore, of critical importance. Such a taxonomy will make it possible to apply common transparency rules on all financial products, resulting in an obligation for all companies to report the proportion of green activities that make up their financial portfolios. Such a taxonomy could be based on discriminating thresholds for factors such as carbon emissions, and could take into account the no-harm principle in order to define which projects count as green. However, ongoing debates on nuclear energy (JRC, 2021[31]) are testament to the complexity of implementing this taxonomy, which is nevertheless of primordial importance for identifying and supporting green investments. A binary classification of projects into low-carbon and high-carbon may, however, not be possible nor beneficial from the perspective of financial market participants. It may therefore be acceptable to assume that certain projects will lay in-between these two categories.

Additionally, stronger benchmarks and taxonomies to evaluate environmental, social and corporate governance (ESG) performance in the financial sector may also facilitate green financing and reduce reliance on ESG rating and research providers (OECD, 2020[21]). Various core approaches to ESG investing exist, including negative and positive screening, tilting investment portfolios aligned with ESG scores, as well as ESG impact and integration practices. Combined with different investment strategies, these approaches could alter asset selection in portfolios. Furthermore, the lack of standardised reporting practices and transparency, combined with the difficulty to translate qualitative information into quantitative facts, hinders the proper integration of climate-related factors into investment decisions (Boffo and Patalano, 2020[32]). It is also important to align industry-based (i.e. rating providers) environmental scores with composite ESG scores in order to meet investors’ environmental expectations. At the same time, environmental and ESG scores need to be carefully interpreted. High-ESG portfolios may not necessarily reflect a strong environmental performance or low-carbon activities. In turn, investors will need to conduct more thorough due diligence to get a better understanding of whether the scores of the rating provider properly incorporate and weigh such factors (Boffo, Marshall and Patalano, 2020[33]).

Some ASEAN member states have provided guidance on eligible project categories for green finance. Moreover, ASEAN’s framework of specific standards for green, social, or sustainability-related bonds are commonly used by member states to label a new bond or sukuk. These standards are based on the International Capital Market Association’s principles and guidelines (ASEAN, 2020[34]). In 2019, meanwhile, the Malaysian central bank issued a discussion paper on climate change and its impact on the financial system. It serves as a guide for financial institutions practices in identifying and classifying the economic activities that could contribute to climate change objectives (BNM, 2019[35]).

In 2015, the central bank of China published an endorsed project catalogue for green bonds, which is applicable to financial institutions and listed companies that want to issue them. Since then, several green standards and classification methods have been issued by various ministries and commissions in China, as well as by regional authorities, including, the China Securities Regulatory Commission (CSRC), the National Development and Reform Commission (NDRC), and the China Banking and Insurance Regulatory Commission. The taxonomies issued by the various bodies are to a large extent similar, although slight differences can be identified. In May 2020, the central bank, along with the NDRC and the CSRC, submitted a new edition of their project-support directory for green bonds, in a bid to harmonise the different taxonomies used by different government agencies (World Bank, 2020[36]).

At the regional level, central banks have worked together to develop the ASEAN Central Banks’ Agenda on Sustainable Banking. The agenda provides guidance to participants on ways to safeguard financial stability while at the same time supporting the transition to a low-carbon economy. Among other recommendations, central banks may collectively explore the development of a common, principles-based, ASEAN-wide taxonomy, along with specific green lending principles, in order to channel capital towards environmentally friendly activities. The common agenda on sustainable banking also promotes the establishment of a data collection framework. The goals of this framework are to ensure the proper monitoring of risk exposures, and to facilitate the assessment of the financial sector’s vulnerability to climate and environment-related risks (ASEAN, 2020[37]).

These initiatives notwithstanding, there is currently no common regional taxonomy or classification system for green finance in Emerging Asia. The European Union’s Taxonomy Regulation, which has been applicable in member states since June 2020, could provide a useful reference point for policy makers in Emerging Asia. It is a classification system that establishes a list of environmentally sustainable economic activities. Furthermore, it provides appropriate definitions to companies, investors, and policy makers on which economic activities can be considered environmentally sustainable. The overarching goal of the EU’s green classification system is to create security for investors, protect private investors from “greenwashing”, help companies plan the transition to a low-carbon economy, mitigate market fragmentation, and eventually help shift investments to where they are most needed. Box 2.3 contains more details about the guiding principles of the EU taxonomy for environmentally sustainable economic activities.

The taxonomy defines the environmental performance characteristics that economic activities must achieve in order to make a significant contribution to one of the following six environmental objectives: 1) climate change mitigation; 2) climate change adaptation; 3) the sustainable use and protection of water and marine resources; 4) the transition to a circular economy; 5) pollution prevention and control; and 6) the protection and restoration of biodiversity and ecosystems.

In order to be applicable to a large number of sectors, the EU taxonomy distinguishes between several types of contribution to environmental objectives. Some activities, such as electricity production from solar or wind power, make a positive contribution to these objectives by default. Others, such as steel production, make a contribution to the transition under certain conditions. Finally, a third category brings together activities which allow other operations to achieve environmental objectives, such as the production of batteries or solar panels.

The EU Taxonomy Regulation targets three groups of users: 1) financial-market participants offering financial products in the European Union, including occupation pension providers; 2) large companies that are already required to provide a non-financial statement under the EU’s Non-Financial Reporting Directive; and 3) the EU institutions and member states, when setting public measures, standards, or labels for green financial products or green (corporate) bonds. Financial-market participants will be required to complete their first set of disclosures against the EU taxonomy, covering activities that substantially contribute to climate change mitigation and/or adaptation, by 31 December 2021. For their part, companies listed at point (2) will be required to disclose several financial metrics (Table 2.10) over the course of 2022.

Source: European Commission (2020[38]), Taxonomy: Final report of the Technical Expert Group on Sustainable Finance, European Commission, Brussels, .

This chapter provides several analytical insights into the role that macroprudential policy could play in supporting the transition from a high-carbon to a low-carbon economy. Two broad aspects must be taken into account in this regard. The first of these is related to identifying macroprudential requirements that could hinder the transition to a low carbon economy. The second important question is how to enhance the existing macroprudential framework to better manage climate-related risks, and to promote investment in green assets and activities over brown ones.

More could be done to enhance the financial sector’s role in allocating capital in support of a low-carbon transition. Notwithstanding the development of green finance, there is still a large investment gap. In addition, financial institutions have yet to fully consider the risks associated with climate change, namely physical and transition risks. For various reasons, the financial sector has not sufficiently transformed its business model to finance the low-carbon transition, and to manage risks effectively in order to avoid being impacted by climate change itself. While financial market participants appear to be using the information available to them to start pricing in the low-carbon transition, this attempt is currently hampered by insufficient data and analytical tools to measure and manage climate transition risks.

Against this background, this chapter has shown there are good reasons to believe macroprudential policy must push the financial sector to provide a quick response to the challenges of climate change, and to play its role in the green transition. In this regard, macroprudential authorities in Emerging Asia need to bolster their tools for monitoring systemic risk, in order to better anticipate the impact of climate change on the financial sector. One way that they could achieve this is through climate-related stress tests. Furthermore, authorities could consider amending some existing macroprudential policy tools. This would be a way to limit certain carbon-intense activities, by applying differentiated capital requirements on green assets and activities versus brown ones. At the same time, it would be possible to make sure that these requirements do not hamper the green transition. This could be done by ensuring that the minimum liquidity requirements to which banks are subject do not discourage the financing of long-term green investments. The development of a taxonomy for the identification of green assets and activities versus brown ones, possibly at the regional level, is a prerequisite for the effective conduct of green macroprudential policy. It will be equally important to provide guidance on the classification of projects that lie on the spectrum between green and brown to reflect the reality that certain projects may not be easily assigned to one of the two categories.

References

[12] ADB (2021), Asian Development Outlook 2021: Financing a Green and Inclusive Recovery, Asian Development Bank, Manila, http://dx.doi.org/10.22617/fls210163-3.

[6] AIIB/Amundi (2020), “Climate Change Investment Framework”, AIIB Asia Climate Bond Portfolio Case Study, Asian Infrastructure Investment Bank/Amundi, https://www.aiib.org/en/policies-strategies/framework-agreements/climate-change-investment-framework/.content/index/AIIB-Amundi-Climate-Change-Investment-Framework-FINAL-VERSION.pdf.

[37] ASEAN (2020), ASEAN Central Banks’ Agenda on Sustainable Banking, Association of Southeast Asian Nations, Jakarta, https://asean.org/storage/2020/10/Annex-ASEAN-Central-Banks-Agenda-on-Sustainable-Banking-002.pdf.

[34] ASEAN (2020), Report on promoting sustainable finance in ASEAN, Association of Southeast Asian Nations, Jakarta, https://asean.org/storage/2012/05/Report-on-Promoting-Sustainable-Finance-in-ASEAN-for-AFCDM-AFMGM.pdf.

[22] Batten, S., R. Sowerbutts and M. Tanaka (2016), “Let’s talk about the weather: The impact of climate change on central banks”, Staff Working Papers, No. 603, Bank of England, London, https://www.bankofengland.co.uk/-/media/boe/files/working-paper/2016/lets-talk-about-the-weather-the-impact-of-climate-change-on-central-banks.pdf?la=en&hash=C49212AE5F68EC6F9E5AA71AC404B72CDC4D7574.

[35] BNM (2019), Climate Change and Principle-based Taxonomy, Bank Negara Malaysia, Kuala Lumpur, http://www.bnm.gov.my/documents/20124/938039/Climate+Change+and+Principle-based+Taxonomy.pdf.

[33] Boffo, R., C. Marshall and R. Patalano (2020), ESG Investing: Environmental Pillar Scoring and Reporting, OECD, Paris, https://www.oecd.org/finance/ESG-Investing-Environmental-Pillar-Scoring-and-Reporting.pdf.

[32] Boffo, R. and R. Patalano (2020), ESG Investing: Practices, Progress and Challenges, OECD, Paris, https://www.oecd.org/finance/ESG-Investing-Practices-Progress-Challenges.pdf.

[10] Bolton, P. et al. (2020), The Green Swan: Central Banking and Financial Stability in the Age of Climate Change, Bank for International Settlements, Basel, Switzerland, https://www.bis.org/publ/othp31.pdf.

[30] Campiglio, E. et al. (2018), “Climate change challenges for central banks and financial regulators”, Nature Climate Change, Vol. 8/6, pp. 462-468, http://dx.doi.org/10.1038/s41558-018-0175-0.

[1] Dikau, S. and U. Volz (2021), “Central bank mandates, sustainability objectives and the promotion of green finance”, Ecological Economics, Vol. 184, p. 107022, http://dx.doi.org/10.1016/j.ecolecon.2021.107022.

[23] Dikau, S. and U. Volz (2018), “Central Banking, Climate Change and Green Finance”, No. 867, Asian Development Bank Institute, Tokyo, https://core.ac.uk/download/pdf/161527987.pdf.

[28] D’Orazio, P. and L. Popoyan (2019), “Dataset on green macroprudential regulations and instruments: Objectives, implementation and geographical diffusion”, Data in Brief, Vol. 24, p. 103870, http://dx.doi.org/10.1016/j.dib.2019.103870.

[25] D’Orazio, P. and L. Popoyan (2019), “Fostering green investments and tackling climate-related financial risks: Which role for macroprudential policies?”, Ecological Economics, Vol. 160, pp. 25-37, http://dx.doi.org/10.1016/j.ecolecon.2019.01.029.

[29] EBA (2019), EBA report on undue short-term pressure from the financial sector on corporations, European Banking Authority, Frankfurt, https://www.eba.europa.eu/sites/default/documents/files/document_library/Final%20EBA%20report%20on%20undue%20short-term%20pressures%20from%20the%20financial%20sector%20v2_0.pdf.

[9] ECB (2020), Guide on climate-related and environmental risks: Supervisory expectations relating to risk management and disclosure, European Central Bank, Frankfurt, https://www.bankingsupervision.europa.eu/ecb/pub/pdf/ssm.202011finalguideonclimate-relatedandenvironmentalrisks~58213f6564.en.pdf.

[38] European Commission (2020), Taxonomy: Final report of the Technical Expert Group on Sustainable Finance, European Commission, Brussels, https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/200309-sustainable-finance-teg-final-report-taxonomy_en.pdf.

[20] Fitch Ratings (2021), Climate Stress Tests to Be Mainstream for Banks, Insurers, Fitch Ratings, London, https://www.fitchratings.com/research/banks/climate-stress-tests-to-be-mainstream-for-banks-insurers-15-03-2021.

[15] Gersbach, H. and J. Rochet (2012), “Aggregate Investment Externalities and Macroprudential Regulation”, Journal of Money, Credit and Banking, Vol. 44, Supplement 2, Wiley, Hoboken, New Jersey, pp. 73-109, https://www.jstor.org/stable/23321957.

[14] IFC (2018), Raising US$23 Trillion: Greening Banks and Capital Markets for Growth, International Finance Corporation, World Bank Group, Washington D.C., http://documents1.worldbank.org/curated/en/995131540533377620/pdf/131346-WP-Greening-Banks-CapitalMkts-PUBLIC.pdf.

[31] JRC (2021), Technical assessment of nuclear energy with respect to the ‘do no significant harm’ criteria of Regulation (EU) 2020/852 (‘Taxonomy Regulation’), Joint Research Centre of the European Commission, Brussels, https://ec.europa.eu/info/sites/info/files/business_economy_euro/banking_and_finance/documents/210329-jrc-report-nuclear-energy-assessment_en.pdf.

[7] Luo, T. and G. Christianson (2018), Water Shortages Cost Indian Energy Companies Billions, World Resources Institute, Washington, D.C., https://www.wri.org/insights/water-shortages-cost-indian-energy-companies-billions.

[19] MAS (2020), Reply to Parliamentary Question on including climate change-related risk in MAS’ annual industry-wide stress test, Monetary Authority of Singapore, https://www.mas.gov.sg/news/parliamentary-replies/2020/reply-to-parliamentary-question-on-including-climate-change-related-risk-in-mas-annual-iwst.

[17] Narbel, P. (2013), “The likely impact of Basel III on a bank’s appetite for renewable energy financing”, Discussion papers, Norwegian School of Economics, Bergen, Norway, https://core.ac.uk/download/pdf/52096366.pdf.

[4] NGFS (2019), A call for action: Climate change as a source of financial risk, Central Banks and Supervisors Network for Greening the Financial System, Banque de France, Paris, https://www.ngfs.net/sites/default/files/medias/documents/ngfs_first_comprehensive_report_-_17042019_0.pdf.

[3] NGFS (2018), First Progress Report October 2018, Central Banks and Supervisors Network for Greening the Financial System, Banque de France, Paris, https://www.banque-france.fr/sites/default/files/media/2018/10/11/818366-ngfs-first-progress-report-20181011.pdf.

[21] OECD (2020), OECD Business and Finance Outlook 2020: Sustainable and Resilient Finance, OECD Publishing, Paris, https://dx.doi.org/10.1787/eb61fd29-en.

[27] Park, H. and J. Kim (2020), “Transition towards green banking: role of financial regulators and financial institutions”, Asian Journal of Sustainability and Social Responsibility, Vol. 5/1, http://dx.doi.org/10.1186/s41180-020-00034-3.

[5] PRA (2019), Life Insurance Stress Test 2019: Scenario Specification, Guidelines and Instructions, Prudential Regulation Authority, Bank of England, London, https://www.bankofengland.co.uk/-/media/boe/files/prudential-regulation/letter/2019/life-insurance-stress-test-2019-scenario-specification-guidelines-and-instructions.pdf.

[26] RBI (2020), Master Directions – Priority Sector Lending (PSL) – Targets and Classification, Reserve Bank of India, New Delhi, https://rbidocs.rbi.org.in/rdocs/notification/PDFs/MDPSL803EE903174E4C85AFA14C335A5B0909.PDF.

[24] Schoenmaker, D. and R. Van Tilburg (2016), “What Role for Financial Supervisors in Addressing Environmental Risks?”, Comparative Economic Studies, Vol. 58/3, pp. 317-334, http://dx.doi.org/10.1057/ces.2016.11.

[18] Spencer, T. and J. Stevenson (2013), “EU Low-Carbon Investment and New Financial Sector Regulation: What Impacts and What Policy Response?”, IDRI Working Papers, No. 5, Sciences Po, Paris, https://www.iddri.org/sites/default/files/import/publications/wp0513_ts-js_financial-regulation.pdf.

[8] Suhartono, H. (2020), “Carmakers Seek Relief to Indonesia Emission Rules Amid Pandemic”, Bloomberg News, Bloomberg, https://www.bloomberg.com/news/articles/2020-05-13/carmakers-seek-relief-to-indonesia-emission-rules-amid-pandemic (accessed on 29 May 2021).

[2] TCFD (2017), “Recommendations of the Task Force on Climate-related Financial Disclosures”, Task Force on Climate-Related Financial Disclosures, Bank for International Settlements, Basel, Switzerland, https://assets.bbhub.io/company/sites/60/2020/10/FINAL-2017-TCFD-Report-11052018.pdf.

[16] Thanassoulis, J. (2014), “Bank pay caps, bank risk, and macroprudential regulation”, Journal of Banking & Finance, Vol. 48, pp. 139-151, http://dx.doi.org/10.1016/j.jbankfin.2014.04.004.

[11] Vermeulen, R. et al. (2018), “An energy transition risk stress test for the financial system of the Netherlands”, Occasional Studies, Vol. 16. No. 7, De Nederlandsche Bank, Amsterdam, https://www.dnb.nl/media/pdnpdalc/201810_nr-_7_-2018-_an_energy_transition_risk_stress_test_for_the_financial_system_of_the_netherlands.pdf.

[13] Volz, U. (2018), “Fostering Green Finance for Sustainable Development in Asia”, ADBI Working Papers, No. 814, Asian Development Bank Institute, Tokyo, https://www.adb.org/sites/default/files/publication/403926/adbi-wp814.pdf.

[36] World Bank (2020), Developing a National Green Taxonomy, A World Bank Guide, World Bank Group, Washington D.C., http://documents1.worldbank.org/curated/en/953011593410423487/pdf/Developing-a-National-Green-Taxonomy-A-World-Bank-Guide.pdf.

Collaboratively administrate empowered markets via plug-and-play networks. Dynamically procrastinate B2C users after installed base benefits. Dramatically visualize customer directed convergence without

Comments