Basel framework and basel 3 framework

Posted by: admin 2 years, 7 months ago

(Comments)

Basel Framework

The Basel Framework is the full set of standards of the Basel Committee on Banking Supervision (BCBS), which is the primary global standard-setter for the prudential regulation of banks. The membership of the BCBS has agreed to fully implement these standards and apply them to the internationally active banks in their jurisdictions.

About BIS

BIS, or Bank for International Settlements, was founded at a meeting held by representatives from central banks across Europe in 1930. Its mission is "to promote international cooperation among central bankers". It does this through its work as an independent institution that provides policy advice, research and analysis; it also acts as a bank supervisor for member countries' banking systems. Committees & associations

Committees & associations BIS committees are composed of leading academics from around the world who provide independent advice to the Bank in its work with governments and other institutions.

Governance

Governance The Board of Directors oversees the management of the Bank by ensuring that it operates effectively within Central the bank framework hub

The set Central out Bank by Hub provides statutes. information It also ensures work that of the policies world’s adopted leading by central the banks. Bank It includes consistent data with on those nationally agreed policies, upon statistics, at news meetings releases, of speeches the by Governing senior Council.

officials, working papers, studies and more.

Media working or & with the speeches countries Board BIS around of staff the Governors regularly world of comment since the on 1945 Federal developments to Reserve affecting help System. them world achieve economy macroeconomic at policies news consistent conferences with or their media economic interviews development around objectives.

The Basel final Committee rule on requires Banking that Supervision all was banking established organizations in with 1988 total by consolidated the gross Bank exposures for exceeding International 3 Settlements, per cent an of international GDP organization maintain that a promotes additional sound tier-one money capital policies buffer and equal practices to among at central least banks 2 worldwide. per cent The of BCBS such has exposure developed above guidelines certain known thresholds. as “Principles” which are intended to provide guidance to financial institutions regarding their capital requirements. These principles were first published in 1996 and have been revised several times since then.

The fundamental goal of the Basel Committee was to further strengthen the soundness and stability of the international banking system. (bundesbank.de)

History about Basel

- Basel I: 1988–1999

- Basel II: 2004–2013

- Basel III: 2013 onwards

Basel I

Basel II

Basel II included new regulatory additions and was centred around improving three key issues – minimum capital requirements, supervisory mechanisms and transparency, and market discipline. (corporatefinanceinstitute.com)

Basel III

Banking regulation framework Basel III is a global, voluntary regulatory framework on bank capital adequacy stress testing market liquidity risk. This third instalment of the Basel Accords Basel I Basel II ) was developed in response to the deficiencies in financial regulation revealed by the financial crisis of 2007–08. The new rules will require banks to hold more equity than before, but they are not as stringent as those proposed under Basel II, which would have required them to increase their common stockholders' equity ratio to 8% for large institutions and 6% What for Is smaller Basel ones. III?

Minimum Capital Requirements The Basel III accord raised the minimum capital requirements for banks from 2% in Basel II to 4.5% of common equity, as a percentage of the bank's risk-weighted assets. (corporatefinanceinstitute.com)

Information about Basel III in brief

- Basel III transitional arrangements, 2017-2028

- Basel III summary table

- Finalising Basel III - in brief

- The market risk framework - in brief

Basel III summary table

An important aspect is

Afftecting all bank and SIBS (systematically international bank)

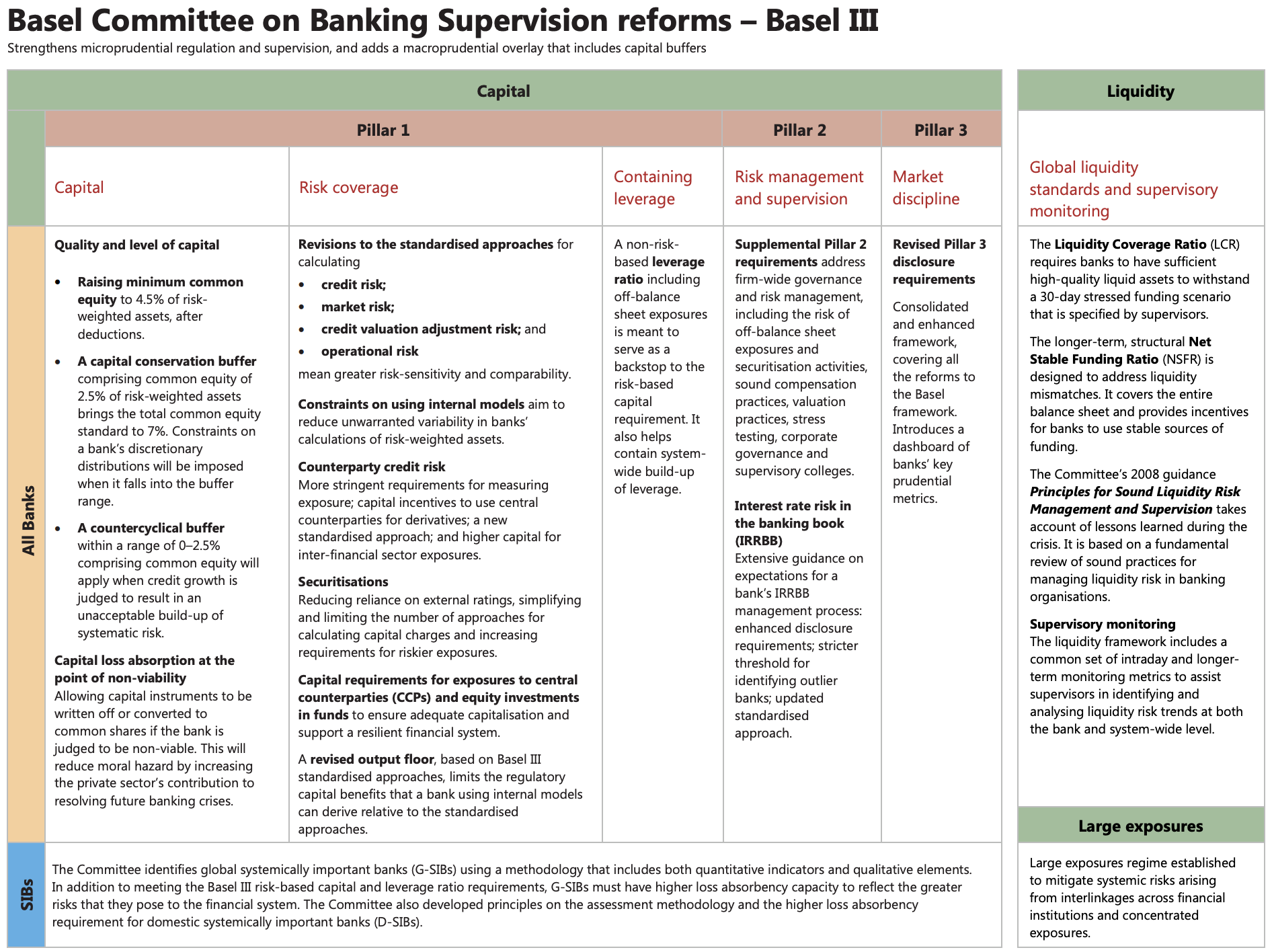

Capital

- Pillar 1 (Capital)

- Capital (Quality and level of capital)

- Capital (Quality and level of capital)

- Raising minimum common equity to 4.5% of risk-weighted assets, after deductions. •

- A capital conservation buffer comprising common equity of 2.5% of risk-weighted assets brings the total common equity standard to 7%. Constraints on a bank’s discretionary distributions will be imposed when it falls into the buffer range. •

- A countercyclical buffer within a range of 0–2.5% comprising common equity will apply when credit growth is judged to result in an unacceptable build-up of systematic risk.

- Capital loss absorption at the point of non-viability Allowing capital instruments to be written off or converted to common shares if the bank is judged to be non-viable. This will reduce moral hazard by increasing the private sector’s contribution to resolving future banking crises.

- Capital (Quality and level of capital)

- Risk coverage

- Revisions to the standardised approaches for calculating •

- credit risk; •

- market risk; •

- credit valuation adjustment risk; and •

- operational risk means greater risk sensitivity and comparability.

- Constraints on using internal models aim to reduce unwarranted variability in banks’ calculations of risk-weighted assets.

- Counterparty credit risk More stringent requirements for measuring exposure; capital incentives to use central counterparties for derivatives; a new standardised approach; and higher capital for inter-financial sector exposures.

- Securitisations Reducing reliance on external ratings, simplifying and limiting the number of approaches for calculating capital charges and increasing requirements for riskier exposures.

- Capital requirements for exposures to central counterparties (CCPs) and equity investments in funds to ensure adequate capitalisation and support a resilient financial system.

- A revised output floor, based on Basel III standardised approaches, limits the regulatory capital benefits that a bank using internal models can derive relative to the standardised approaches

- Revisions to the standardised approaches for calculating •

- Containing leverage

- A non-risk-based leverage ratio including off-balance sheet exposures is meant to serve as a backstop to the risk-based capital requirement. It also helps contain the systemwide build-up of leverage.

- Capital (Quality and level of capital)

- Pillar 2

- Supplemental Pillar 2 requirements address firm-wide governance and risk management, including the risk of off-balance sheet exposures and securitisation activities, sound compensation practices, valuation practices, stress testing, corporate governance and supervisory colleges.

- Interest rate risk in the banking book (IRRBB) Extensive guidance on expectations for a bank’s IRRBB management process: enhanced disclosure requirements; the stricter threshold for identifying outlier banks; updated standardised approach.

- Pillar 3

- Revised Pillar 3 disclosure requirements Consolidated and enhanced framework, covering all the reforms to the Basel framework. Introduces a dashboard of banks’ key prudential metrics.

Basel 3 explanation on video

SIBS

The Committee identifies global systemically important banks (G-SIBs) using a methodology that includes both quantitative indicators and qualitative elements. In addition to meeting the Basel III risk-based capital and leverage ratio requirements, G-SIBs must have higher loss absorbency capacity to reflect the greater risks that they pose to the financial system. The Committee also developed principles on the assessment methodology and the higher loss absorbency requirement for domestic systemically important banks (D-SIBs).

Liquidity

- Global liquidity standards and supervisory monitoring

- The Liquidity Coverage Ratio (LCR) requires banks to have sufficient high-quality liquid assets to withstand a 30-day stressed funding scenario that is specified by supervisors.

- The longer-term, structural Net Stable Funding Ratio (NSFR) is designed to address liquidity mismatches. It covers the entire balance sheet and provides incentives for banks to use stable sources of funding.

- The Committee’s 2008 guidance Principles for Sound Liquidity Risk Management and Supervision takes account of lessons learned during the crisis. It is based on a fundamental review of sound practices for managing liquidity risk in banking organisations.

- Supervisory monitoring The liquidity framework includes a common set of intraday and longer-term monitoring metrics to assist supervisors in identifying and analysing liquidity risk trends at both the bank and system-wide levels.

- Large exposures

- Large exposures regime established to mitigate systemic risks arising from interlinkages across financial institutions and concentrated exposures.

the International globe.

out An what's independent happening organization at based the in Bank Geneva, for Switzerland, International ISO Settlements develops by voluntary following consensus our The standards latest Basel worldwide. press Framework

The releases Basel and framework announcements.

Stress test on capital video

Last update about Basel

The Commission Basel for Committee Europe

on Banking Supervision is a committee of the Bank for International Settlements, an international organization that promotes central banking and financial stability. The BCBS was established in 1930 by the Basle Accords to regulate capital adequacy requirements for banks worldwide. It has since been responsible for setting minimum standards for bank regulation around the world. CET1 capital requirements

This measure intends to restrict the build-up of leverage in the banking sector and reinforce the risk-based requirements with a simple, non-risk-based "backstop" measure. (bis.org)

Innovation and fintech Coronavirus (Covid-19) Climate change & green finance BIS authors Annual Economic Report Quarterly Review Working Group on Financial Stability Other publications Committees & associations Committees & associations The BIS hosts nine international organisations engaged in standard setting and the pursuit of financial stability through the Basel Process. (bis.org)

Criticisms The Institute of International Finance, a 450-member banking trade association located in the United States, protested the implementation of Basel III due to its potential to hurt banks and slow down economic growth. (corporatefinanceinstitute.com)

Share on Twitter Share on Facebook

3 months ago

A reflection of using kanban flow and being minimalist

Recent newsToday is the consecutive day I want to use and be consistent with the Kanban flow! It seems it's perfect to limit my parallel and easily distractedness.

read more3 months, 1 week ago

3 months, 2 weeks ago

Podcast Bapak Dimas 2 - pindahan rumah

Recent newsVlog kali ini adalah terkait pindahan rumah!

read more3 months, 2 weeks ago

Podcast Bapak Dimas - Bapaknya Jozio dan Kaziu - ep 1

Recent newsSeperti yang saya cerita kan sebelumnya, berikut adalah catatan pribadi VLOG kita! Bapak Dimas

read more3 months, 2 weeks ago

Happy new year 2024 and thank you 2023!

Recent newsAs the new year starts, I want to revisit what has happened in 2023.

read more3 months, 2 weeks ago

Some notes about python and Zen of Python

Recent newsExplore Python syntax

Python is a flexible programming language used in a wide range of fields, including software development, machine learning, and data analysis. Python is one of the most popular programming languages for data professionals, so getting familiar with its fundamental syntax and semantics will be useful for your future career. In this reading, you will learn about Python’s syntax and semantics, as well as where to find resources to further your learning.

4 months, 4 weeks ago

Collaboratively administrate empowered markets via plug-and-play networks. Dynamically procrastinate B2C users after installed base benefits. Dramatically visualize customer directed convergence without

Comments